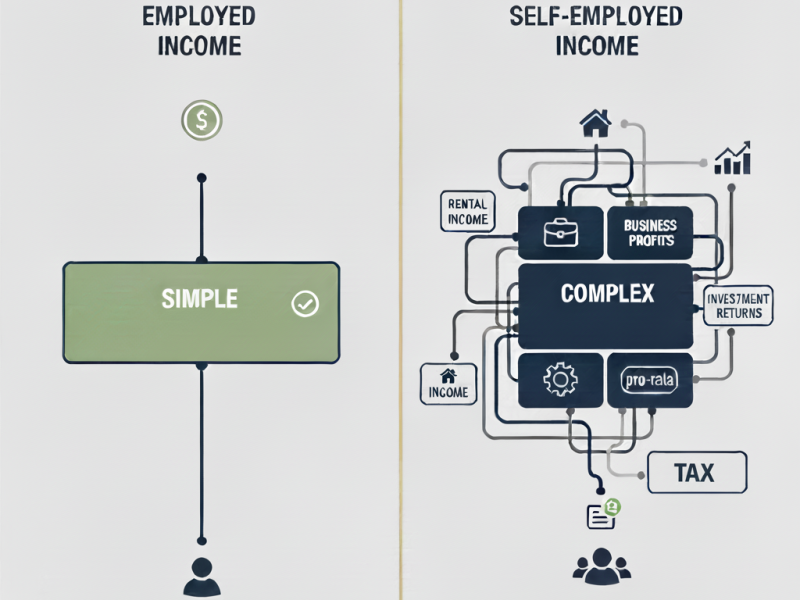

featIf you’re a business owner or self-employed professional facing divorce in New York, calculating child support is more complex than for W-2 employees. Your income fluctuates, business expenses blur the lines between professional and personal, and tax returns don’t always tell the complete story. Understanding how New York approaches self-employment income is essential to reaching a fair agreement.

How New York Defines Income for Self-Employed Parents

In New York, child support calculations use Child Support Standards Act income. For business owners, this includes all business income before expenses are deducted—wages or salary you pay yourself, business profits or distributions, and any other compensation from business operations.

The starting point is your tax returns: Schedule C for sole proprietors, or K-1s for partnerships and S corporations. However, tax returns aren’t the final word.

New York applies percentages to combined parental income up to $183,000: 17 percent for one child, 25 percent for two, 29 percent for three, increasing for additional children. For income above $183,000, treatment becomes a matter for negotiation based on the children’s needs.

The Add-Back Question: What Business Expenses Count?

Not every expense that reduces your taxable income for IRS purposes reduces your income for child support purposes in New York. The state adds explicitly back certain self-employment deductions that provide personal benefits.

New York law explicitly addresses two categories. First, depreciation deductions that exceed straight-line depreciation get added back. If you’re using accelerated depreciation methods to reduce your taxable income faster than the asset actually loses value, that excess gets added back for child support purposes.

Second, entertainment and travel allowances get added back to the extent they reduce your personal expenditures. If you’re deducting business meals you would have eaten anyway, travel that combines business with personal vacation, or vehicle expenses for a car you drive for both business and personal use, the portion providing personal benefit gets added back.

Beyond these statutory add-backs, what counts as reasonable versus unreasonable business expenses becomes a key negotiation point. Equipment purchases that genuinely expand your business capacity are typically accepted as legitimate. Salaries paid to family members who perform actual work at market rates are generally considered reasonable. Professional fees, insurance, and operational costs necessary to run your business usually aren’t questioned.

However, excessive expenses that seem designed to reduce your apparent income artificially raise concerns. Paying yourself a minimal salary while reinvesting heavily in the business right before or during divorce proceedings invites scrutiny. Suddenly deducting large amounts for equipment or renovations that weren’t part of your regular pattern creates suspicion. Running personal expenses through your business account undermines your credibility.

The Lifestyle Analysis Reality

Lifestyle analysis compares your actual living expenses against reported income. If you report earning $50,000 annually but maintain a $4,000 monthly mortgage, drive a luxury vehicle, and live a $100,000 lifestyle, the numbers don’t match. Bank statements and spending patterns reveal what your income actually supports.

This isn’t about catching people in lies. Business owners sometimes don’t realize how much personal benefit flows through business deductions—such as cell phones, vehicles, meals, and home offices. That’s thoughtful tax planning, but those benefits represent real income for child support purposes.

Why Documentation Matters

Thorough documentation is your most important asset. The burden of proving your income rests on you as the business owner.

You’ll need at least 3 years of personal and business tax returns, including all schedules. Profit and loss statements prepared by an accountant carry more weight. Bank statements for business and personal accounts help complete the picture. Corporate entities need to file corporate tax returns and prepare financial statements.

Clear separation between business and personal expenses protects you. Mixing personal purchases into business accounts or paying yourself irregularly creates ambiguity that rarely works in your favor.

For variable income businesses, multiple years establish patterns. If your income genuinely fluctuates based on market conditions or projects, documentation is crucial. One unusual year shouldn’t define an ongoing obligation if it doesn’t reflect the typical earning capacity.

How Business Structure Affects Income Evaluation

How your business is structured affects income evaluation. Sole proprietors report via Schedule C, making business income straightforward but requiring careful distinction between legitimate and personal expenses.

Partnerships use K-1 forms to show distributive shares. What matters is what you were entitled to take, not just what you withdrew. Money left in the partnership may still count as available income.

S corporations are unique. You might pay yourself a modest W-2 salary while taking larger distributions. Both get examined. If your salary seems unreasonably low, your income might be attributed to reasonable compensation for your work.

Regardless of structure, how you organize compensation for tax purposes doesn’t necessarily control for child support purposes.

Transparency as Strategy in Mediation

When navigating child support as a business owner, transparency is your most effective strategy.

Attempting to hide income or inflate expenses typically backfires. The tools for uncovering financial manipulation are sophisticated, and consequences extend beyond paying correct support. Discovery destroys credibility on every divorce issue.

More importantly, manipulation creates adversarial dynamics that make mediation impossible. Once trust breaks, you’re headed for litigation, where you lose control and spend more.

In mediation, complete transparency creates productive negotiation. When both parents see the whole financial picture, honest conversations about reasonable support become possible. You can discuss averaging variable income, distinguishing necessary from discretionary expenses, and handling legitimate reinvestment needs.

With my finance background and MBA, I’ve helped business-owning couples navigate these complexities. We analyze financials together, discuss reasonable expenses, and create a shared understanding of available income. This collaborative approach maintains credibility while protecting legitimate business interests.

Practical Approaches for Business Owners

Several strategies help business owners reach fair agreements. Using multiple years of returns to calculate average income smooths fluctuations. If your business is seasonal or project-based, averaging provides accuracy.

Agreeing on reasonable expenses before calculating support saves conflict. Rather than arguing line items, discuss expense categories and reach an agreement on deductions versus add-backs.

Including review provisions in building contracts makes sense for variable-income projects. Annual or biennial reviews with adjustment provisions protect both parents and ensure appropriate support as circumstances evolve.

For businesses that need genuine reinvestment, mediation enables creative solutions. You might base support on actual distributions rather than total income, or agree to higher support when business is strong, with provisions for lean periods. These flexible approaches aren’t available in litigation.

Moving Forward with Confidence

Child support calculations for self-employed parents and business owners in New York require navigating complex financial territory. What counts as income, which expenses are deductible, and how to present your financial picture accurately all require careful consideration and expertise.

Mediation offers a path to work through these complexities while maintaining control over the outcome. Rather than having decisions made for you based on rigid formulas applied to financial information that may not capture your complete situation, you can engage in informed discussions about what’s fair and workable for your family.

With expertise in both financial analysis and mediation, we help business-owning couples create child support agreements that accurately reflect income, account for legitimate business needs, and provide appropriate support for children. The combination of financial acumen and mediation skills allows us to guide you through the technical aspects while facilitating the difficult conversations that arise when finances are complex.

If you’re a business owner facing divorce in New York, the path forward doesn’t have to mean contentious litigation over financial records and arguments about every business expense. Mediation provides an opportunity to approach these issues transparently, negotiate fairly, and reach agreements that work for both parents while adequately supporting your children.

FAQs About New York Child Support

About the Authors – Divorce Mediators You Can Trust

Equitable Mediation Services is a trusted and nationally recognized provider of divorce mediation, serving couples exclusively in California, New Jersey, Washington, New York, Illinois, and Pennsylvania. Founded in 2008, this husband-and-wife team has successfully guided more than 1,000 couples through the complex divorce process, helping them reach amicable, fair, and thorough agreements that balance each of their interests and prioritizes their children’s well-being. All without involving attorneys if they so choose.

At the heart of Equitable Mediation are Joe Dillon, MBA, and Cheryl Dillon, CPC—two compassionate, experienced professionals committed to helping couples resolve divorce’s financial, emotional, and practical issues peacefully and with dignity.

Joe Dillon, MBA – Divorce Mediator & Negotiation Expert

As a seasoned Divorce Mediator with an MBA in Finance, Joe Dillon specializes in helping clients navigate complex parental and financial issues, including:

- Physical and legal custody

- Spousal support (alimony) and child support

- Equitable distribution and community property division

- Business ownership

- Retirement accounts, stock options, and RSUs

Joe’s unique blend of financial acumen, mediation expertise, and personal insight enables him to skillfully guide couples through complex divorce negotiations, reaching fair agreements that safeguard the family’s emotional and financial well-being.

He brings clarity and structure to even the most challenging negotiations, ensuring both parties feel heard, supported, and in control of their outcome. This approach has earned him a reputation as one of the most trusted names in alternative dispute resolution.

Cheryl Dillon, CPC – Certified Divorce Coach & Life Transitions Expert

Cheryl Dillon is a Certified Professional Coach (CPC) and the Divorce Coach at Equitable Mediation. She earned a bachelor’s degree in psychology and completed formal training at The Institute for Professional Excellence in Coaching (iPEC) – an internationally recognized leader in the field of coaching education.

Her unique blend of emotional intelligence, coaching expertise, and personal insight enables her to guide individuals through divorce’s emotional complexities compassionately.

Cheryl’s approach fosters improved communication, reduced conflict, and better decision-making, equipping clients to manage divorce’s challenges effectively. Because emotions have a profound impact on shaping the divorce process, its outcomes, and future well-being of all involved.

What We Offer: Flat-Fee, Full-Service Divorce Mediation

Equitable Mediation provides:

- Full-service divorce mediation with real financial expertise

- Convenient, online sessions via Zoom

- Unlimited sessions for one customized flat fee (no hourly billing surprises)

- Child custody and parenting plan negotiation

- Spousal support and asset division mediation

- Divorce coaching and emotional support

- Free and paid educational courses on the divorce process

Whether clients are facing financial complexities, looking to safeguard their children’s futures, or trying to protect everything they’ve worked hard to build, Equitable Mediation has the expertise to guide them towards the outcomes that matter most to them and their families.

Why Couples Choose Equitable Mediation

- 98% case resolution rate

- Trusted by over 1,000 families since 2008

- Subject-matter experts in the states in which they practice

- Known for confidential, respectful, and cost-effective processes

- Recommendations by therapists, financial planners, and former clients

Equitable Mediation Services operates in:

- California: San Francisco, San Diego, Los Angeles

- New Jersey: Bridgewater, Morristown, Short Hills

- Washington: Seattle, Bellevue, Kirkland

- New York: NYC, Long Island

- Illinois: Chicago, North Shore

- Pennsylvania: Philadelphia, Bucks County, Montgomery County, Pittsburgh, Allegheny County

Schedule a Free Info Call to learn if you’re a good candidate for divorce mediation with Joe and Cheryl.